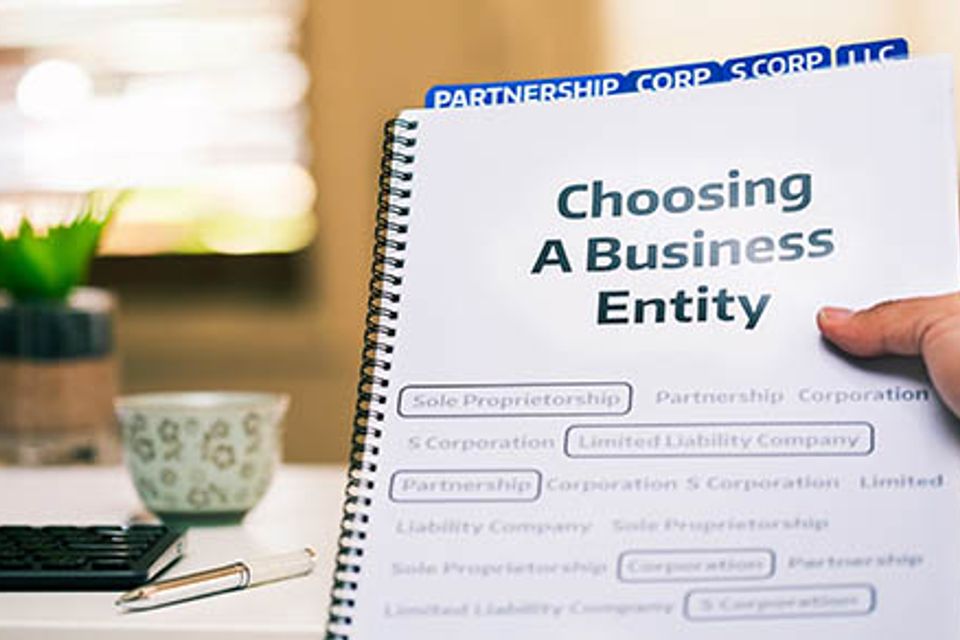

What’s the right entity type for your new business?

Start-ups must choose a legal entity for their business activities. The type of entity you select affects how the business is taxed and who may be held personally liable for its debts and obligations, among other things. Two popular options — assuming you’re going into business with one or more other people — are S corporations and multimember LLCs treated as partnerships for tax purposes. Both are pass-through entities, meaning tax items pass through to the individual owners and are reported on their personal federal income tax returns. And both offer liability protection. But there are subtle differences to factor into your decision. Here’s a closer look at the pros and cons of each.

Multimember LLCs

A multimember LLC essentially combines the legal advantages of corporations with the tax benefits of partnerships. If you operate your business as an LLC, your personal assets are generally protected from exposure to entity-related liabilities under applicable state law. In addition, all LLC members can participate in management without losing their liability protection (unlike partners in a limited partnership). Members of this type of LLC are subject to the federal income tax rules for partners. That means your share of the LLC’s taxable income items, gains, losses, deductions and credits will pass through to you and be reported on your personal return. The LLC itself doesn’t owe federal income tax. In addition to paying income taxes on your share of the LLC’s income, you may owe self-employment tax on that income. This includes Social Security tax at a rate of 12.4% on the first $184,500 of self-employment income in 2026 and Medicare tax of 2.9% on all self-employment income. However, half of your self-employment tax is deductible on your return. It’s also important to note that this business structure isn’t available to all businesses. Certain types of professional practices may be prohibited from operating as LLCs under the laws of some states or applicable professional standards, such as state bar association rules.

S corporations

An S corporation is a special tax designation available to qualifying domestic corporations. Like a traditional C corporation, an S corporation shields its shareholders from personal liability for the corporation’s debts. At the same time, it provides many — though not all — of the tax benefits associated with partnerships. If you structure your start-up as an S corporation, your share of the business’s taxable income items, gains, losses, deductions and credits will pass through to you and be reported on your personal return. The entity itself doesn’t owe federal income tax. S corporations have one important advantage over LLCs treated as partnerships: Shareholder-employees aren’t required to pay self-employment tax on their shares of the profits, provided they receive “reasonable” compensation that’s subject to Social Security and Medicare taxes. However, there are some downsides to consider. Notably, some partnership tax rules that apply to multimember LLCs and their members are significantly more favorable than the rules that apply to S corporations and their shareholders. Here are some examples: LLC members receive additional tax basis for loss deduction purposes from entity-level liabilities, but S corporation shareholders receive additional tax basis only from loans they make to the corporation. This difference allows LLC members to deduct more losses. When an LLC member purchases an interest from another member, the tax basis of the new member’s share of LLC assets can be stepped up. This lowers the new member’s tax obligation when LLC assets are sold or converted to cash. LLCs and their members have greater flexibility to arrange tax-free transfers of assets (including cash) between themselves. In addition, LLCs can make disproportionate allocations of taxable income, losses and other tax items among their members. In contrast, S corporations must allocate all pass-through tax items among the shareholders strictly in proportion to their stock ownership percentages. Also, be aware that not all entities are eligible to make a Subchapter S election. S corporations must comply with strict requirements that limit the number and types of shareholders, prohibit complex capital structures, and impose other restrictions (such as transfers to ineligible shareholders).

Make a tax-smart choice

Choosing your business entity requires careful consideration. Taxes play a pivotal role in this decision. Electing S corporation status or forming an LLC that’s treated as a partnership for tax purposes can provide tax advantages, but only if you structure the entity correctly. Before making your decision, consult with us. We can work with you and your legal advisors to determine the optimal setup for your situation.

Multimember LLCs

A multimember LLC essentially combines the legal advantages of corporations with the tax benefits of partnerships. If you operate your business as an LLC, your personal assets are generally protected from exposure to entity-related liabilities under applicable state law. In addition, all LLC members can participate in management without losing their liability protection (unlike partners in a limited partnership). Members of this type of LLC are subject to the federal income tax rules for partners. That means your share of the LLC’s taxable income items, gains, losses, deductions and credits will pass through to you and be reported on your personal return. The LLC itself doesn’t owe federal income tax. In addition to paying income taxes on your share of the LLC’s income, you may owe self-employment tax on that income. This includes Social Security tax at a rate of 12.4% on the first $184,500 of self-employment income in 2026 and Medicare tax of 2.9% on all self-employment income. However, half of your self-employment tax is deductible on your return. It’s also important to note that this business structure isn’t available to all businesses. Certain types of professional practices may be prohibited from operating as LLCs under the laws of some states or applicable professional standards, such as state bar association rules.

S corporations

An S corporation is a special tax designation available to qualifying domestic corporations. Like a traditional C corporation, an S corporation shields its shareholders from personal liability for the corporation’s debts. At the same time, it provides many — though not all — of the tax benefits associated with partnerships. If you structure your start-up as an S corporation, your share of the business’s taxable income items, gains, losses, deductions and credits will pass through to you and be reported on your personal return. The entity itself doesn’t owe federal income tax. S corporations have one important advantage over LLCs treated as partnerships: Shareholder-employees aren’t required to pay self-employment tax on their shares of the profits, provided they receive “reasonable” compensation that’s subject to Social Security and Medicare taxes. However, there are some downsides to consider. Notably, some partnership tax rules that apply to multimember LLCs and their members are significantly more favorable than the rules that apply to S corporations and their shareholders. Here are some examples: LLC members receive additional tax basis for loss deduction purposes from entity-level liabilities, but S corporation shareholders receive additional tax basis only from loans they make to the corporation. This difference allows LLC members to deduct more losses. When an LLC member purchases an interest from another member, the tax basis of the new member’s share of LLC assets can be stepped up. This lowers the new member’s tax obligation when LLC assets are sold or converted to cash. LLCs and their members have greater flexibility to arrange tax-free transfers of assets (including cash) between themselves. In addition, LLCs can make disproportionate allocations of taxable income, losses and other tax items among their members. In contrast, S corporations must allocate all pass-through tax items among the shareholders strictly in proportion to their stock ownership percentages. Also, be aware that not all entities are eligible to make a Subchapter S election. S corporations must comply with strict requirements that limit the number and types of shareholders, prohibit complex capital structures, and impose other restrictions (such as transfers to ineligible shareholders).

Make a tax-smart choice

Choosing your business entity requires careful consideration. Taxes play a pivotal role in this decision. Electing S corporation status or forming an LLC that’s treated as a partnership for tax purposes can provide tax advantages, but only if you structure the entity correctly. Before making your decision, consult with us. We can work with you and your legal advisors to determine the optimal setup for your situation.